From risk to resilience: The solution slashing banking fraud by 90%

Blog

By Kyle Mallinger, VP: Global Partner & Regional Marketing

I recently caught up with Casey Reynders, SVP, Director of Consumer Product Strategies at Umpqua Bank — our client — and Greg Varnell, VP Product & Development for our partner, Q2.

Along with Entersekt’s VP of Product Development: Identity & Authentication, Mzukisi Rusi, we discussed why financial institutions (FIs), now more than ever, need advanced fraud protection as consumers’ everyday lives continue to be impacted by fraud like account takeovers (ATOs).

The panel explored how to operationalize effective fraud prevention solutions and what success looks like, especially from a customer experience perspective.

Here are a few highlights for FIs that want to build customer trust, especially those seeking innovative authentication solutions on the Q2 platform.

What fraud challenges did Umpqua face before?

During 2024, Umpqua experienced a significant spike in ATO losses, particularly through P2P payments and transfers to linked external accounts. Their biggest concern was the impact on customer trust.

In their search for a solution that could stop fraud in real-time while delivering a good overall customer experience — and be quick and easy to integrate into their existing digital banking platform, Q2 — they found Entersekt.

“The simple combination of strong security, minimal friction, or just enough friction, was really powerful,” explained Reynders.

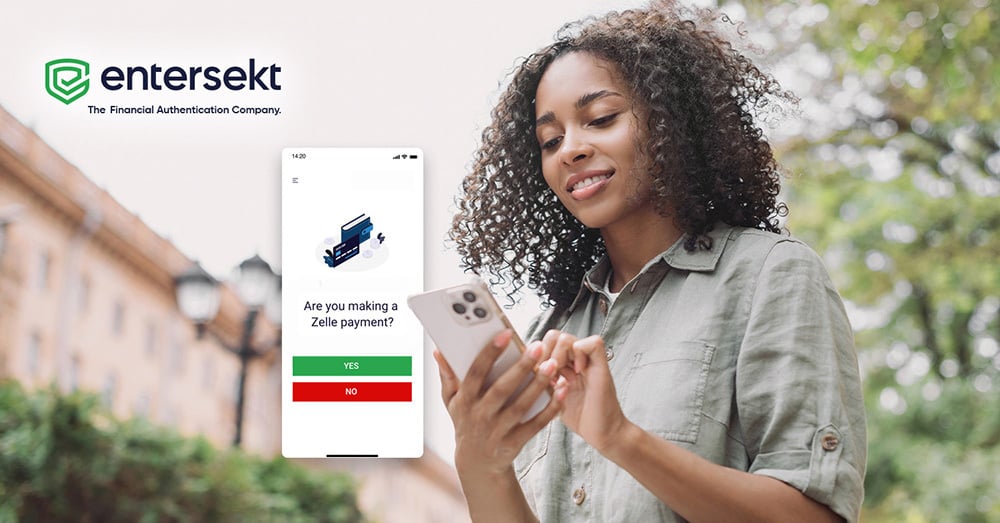

Essentially, by partnering with Entersekt, Umpqua protected its customers' higher-risk payments from attacks like ATO. For P2P and other high-risk transactions, they enabled a push notification to the customer’s trusted device, checking whether it was them about to perform that transaction.

The technology detects and prevents modern fraud threats without subjecting customers to clunky user experiences, which sets the experience apart.

Watch: How Umpqua chose the right Q2 solution partner to prevent rising ATO fraud.

Reducing banking fraud without the usual solution integration headaches

Umpqua Bank implemented Entersekt’s authentication solution through the Q2 platform. And what really stood out was all the work that went into the partnership between the Entersekt and Q2 teams to streamline the process for Umpqua. Essentially, taking the stress out of the development side of the integration, allowing the bank to focus on configuring Entersekt’s solution to their specific business case, like what messages to send to the customer and personalizing the solution with their brand.

A few months after the go-live, when the bank had sufficient data to prove a trend, the impact on their fraud levels was clear – with Casey confirming that regarding their external payment fraud:

“The [Entersekt] promise of 90% reduction has been kept.”

Watch: The impact of Entersekt's solution on the bank's external payment fraud losses.

How can banks balance security and customer experience?

Maintaining a good balance between security that blocks today’s evolving fraud while delivering a great customer experience is an ongoing challenge for many FIs. Entersekt not only helped Umpqua drastically reduce its fraud, but also provided the modern customer experience that the bank was looking for.

While their customers were protected from ATO and other fraud and scam threats, Casey confirmed that with:

While their customers were protected from ATO and other fraud and scam threats, Casey confirmed that with:

“98% of logins and transactions, there’s no visible friction to the user.”

Watch: How intelligent friction helped the bank balance security and customer experience.

How can banks and credit unions keep fraudsters out?

When fraudsters meet friction, they move on. And that’s where Entersekt’s multi-layered authentication approach comes in. It’s no secret that fraud is a big business. Which is why FIs need modern authentication that adds friction for fraudsters.

Platforms like Q2, that link FIs to innovative, effective fraud prevention solutions, help lower the risk profile for their customers, driving fraudsters away to easier targets.

Watch: The impact of friction on fraudsters.

Doesn’t friction frustrate digital banking customers?

In digital banking, we sometimes think friction is a bad thing. But there are times when fraud prevention solutions demand a little bit of friction. Friction in the right place actually builds trust and creates seamless experiences because customers become part of the fight against fraud and feel protected by their FI.

Not all friction is bad. But the solutions FIs choose should drive friction in an intelligent way.

Watch: Why not all friction is bad.

Next steps to strengthen banks’ fraud prevention strategies

Casey highlighted that they waited too long to tackle fraud head on — until after the bank experienced fraud and had to explain the fraud losses to their customers. His final tip for other FIs:

“Don’t do that. Start early and be proactive.”

In other words, step into offense rather than defense mode to improve customer relationships and build trust.

Watch the full webinar to learn more: Click here