When you are based in the U.S., but have employees overseas, purchasing a holiday gift to be delivered to their home can be more challenging than you think. After a year and a half of championing the value of 3-D Secure (3DS) in the fight against card-not-present (CNP) fraud, I recently experienced it firsthand while trying to shop online for my direct reports in South Africa.

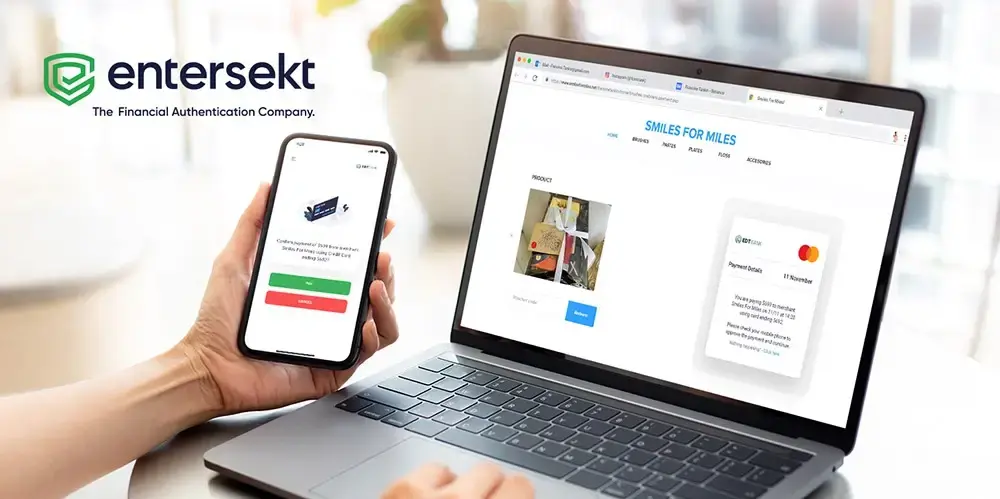

Having a gift shipped from here just didn’t make sense, so I found a suitable local merchant based in Cape Town. After entering my card information, I was actually pleased (and relieved) that my transaction was declined. My card issuer, Chase, immediately notified me by both text and email that a suspicious transaction was attempted on my card.

Having a gift shipped from here just didn’t make sense, so I found a suitable local merchant based in Cape Town. After entering my card information, I was actually pleased (and relieved) that my transaction was declined. My card issuer, Chase, immediately notified me by both text and email that a suspicious transaction was attempted on my card.

3DS builds trust with acceptable friction

The notification provided an option to validate that it was truly me attempting the transaction, or to block that and future transactions. This, to me, is an acceptable level of friction that any consumer would appreciate.

The card issuer recognized that while the purchase was being initiated in the U.S., it was in a geography that was not typical of my card usage (at a merchant in South Africa) and declined the transaction. Whether the transaction triggered their zero-trust approach or whether it was a legitimate fraud step-up measure based on context, I felt protected as a consumer.

And while the transaction took a bit longer, the process went a long way in building additional trust. After verifying that it was me making the purchase, I was able to successfully purchase the gifts and they were delivered the next day!

The card issuer recognized that while the purchase was being initiated in the U.S., it was in a geography that was not typical of my card usage (at a merchant in South Africa) and declined the transaction. Whether the transaction triggered their zero-trust approach or whether it was a legitimate fraud step-up measure based on context, I felt protected as a consumer.

And while the transaction took a bit longer, the process went a long way in building additional trust. After verifying that it was me making the purchase, I was able to successfully purchase the gifts and they were delivered the next day!

3-D Secure adoption rates in North America

While 3DS technology usage has been lagging in the U.S. over concerns of increased user friction and potential transaction abandonment, card issuers, acquirers, and merchants around the world have benefitted from the advantages of the improved EMV 3DS 2.0. These financial institutions process billions of e-commerce transactions through 3DS and advanced authentication capabilities fending off CNP fraud threats at significantly higher rates than in the States.

Looking ahead, here are three reasons why I believe 3DS will gain traction in the U.S. this year:

With so many fraud schemes threatening banks, payment processors, merchants and consumers, these necessary steps should be embraced here in the U.S. as they are across Europe, South Africa and many other countries. We are already seeing early signs that many local financial institutions are anticipating this shift, with many upgrades to more modern 3DS infrastructure planned for 2024.

Looking ahead, here are three reasons why I believe 3DS will gain traction in the U.S. this year:

- The threat was real based on the context of the transaction, which instilled trust.

- The experience was instant and seamless, with authentication options that aligned to my preferences.

- The result was a successful transaction.

With so many fraud schemes threatening banks, payment processors, merchants and consumers, these necessary steps should be embraced here in the U.S. as they are across Europe, South Africa and many other countries. We are already seeing early signs that many local financial institutions are anticipating this shift, with many upgrades to more modern 3DS infrastructure planned for 2024.